(XXXV)...........................WHO CAN BECOME SHAREHOLDER

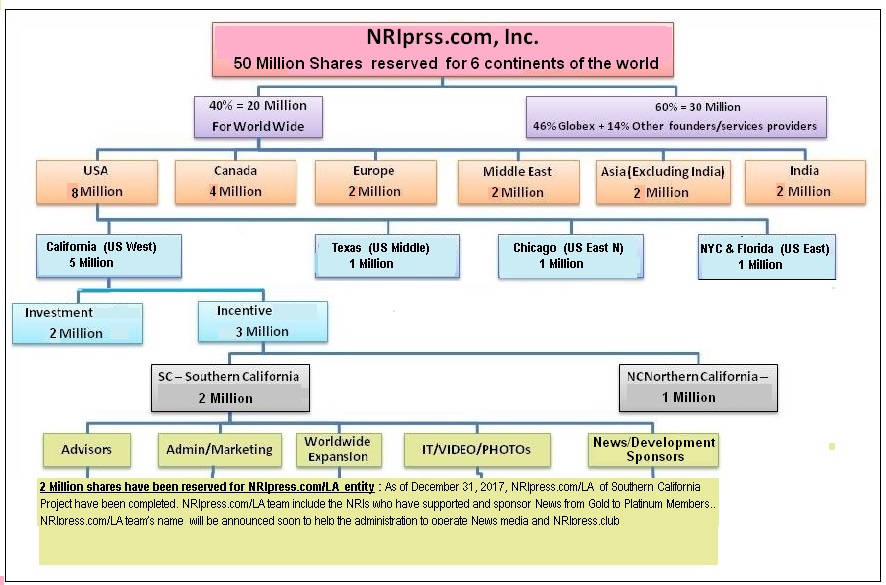

NRIpress.com, Inc.'s Shares Updated, January 01, 2018

- Assume that you paid NRIpress.com Inc., $10,000 (ten thousand $) to sponsor news or advertisement your business within last 10 years or made committment or you offer to provide services towards media next 5 years as an officer........ then you will be eligible to buy (10 times you paid $ amount) upto 100,000 shares with 75% discount under our reserved incentive prog. shares.

|

CLICK FOR FULL CHART |

| SHAREs ISSUE TO | % | ACTUAL SHARES | To WHOME and PURPOSE | ||

| 1 | FOUNDERS | US | 45% | 22.5M | US-Founders--Globex Management- |

| 2 | CO-FOUNDERS | Canada and Asia | 15% | 7.5M | Canada and Asia- Co-Founders |

| 3 | US-IT/Advisors /News supponsors-Model | 10% | 5M | LA -US/Canada Model | |

| 4 | IT | Web Developer | 5% | 2.5M | IT Individual or IT Company who will take full responsibility to develop. Incentive Shares 5 times plus 75% discount (Company can compensate) |

| 5 | Operation | 5% | 2.5M | Run the operation of the projectpIncentive Shares 5 times plus 75% discount (Company can compensate) | |

| 6 | INVESTORS | 10% | 5M | For expansion and update | |

| 7 | RESERVE | 10% | 5M | For Entreprneurs/joint ventures |

IV

The companies or individuals, who like to take NRIpress.com to the next level, two stock options are available:

Incentive Stock Options (ISO):

- ISOs can only be granted to employee

- For ISOs, the benefit flows to the employee — the employee need not pay income taxes on ISOs; instead, assuming the employee holds the options and the stock for the requisite minimum period and meets other conditions,

- The employee is only taxed on the difference between the exercise price and the fair market value at the time of exercise at the long-term capital gains rate (which is lower than the income tax rate).

- Independent contractors must receive non-qualified stock options (NQOs).

- The holders of NQOs must include the value in their income (and must also pay the capital gains tax upon exercise); however, the issuer (employer) may deduct from its own taxes the amount that the option holder must declare in his or her income.

--ISOs and NQOs are IRS classifications, each of which has tax benefits flowing to a different party.